Categories

Financing, Home BuyingPublished June 13, 2025

How to Improve Your Credit Score (Especially If You're Planning to Buy a Home)

Why Your Credit Score Matters When Buying a Home

Thinking about buying a home? One of the first numbers you’ll hear about is your credit score. This three-digit number plays a big role in whether you get approved for a mortgage and what interest rate you’ll pay. A higher score can mean a lower monthly payment, which adds up to big savings over time. If you're planning to buy in the near future, working on your credit should be high on your list.

So, how do you actually improve your credit score? Let’s break it down.

What Is a Credit Score?

Your credit score is a number between 300 and 850. It tells lenders how likely you are to repay borrowed money. The higher the number, the better.

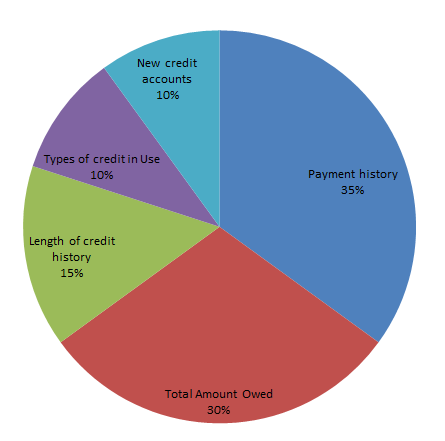

Most mortgage lenders look for a score of at least 620. If you want better loan options and lower rates, aim for 740 or higher. Your score is based on things like payment history, how much debt you have, and how long you’ve had credit. Take a look at the figure below to see what makes up your credit score.

Step-by-Step Tips to Improve Your Credit Score

1. Always Pay Bills on Time

Late payments are one of the fastest ways to damage your credit. On the flip side, paying everything on time builds strong history.

Let’s say your credit card bill is due on the 15th of every month. Setting up automatic payments or reminders on your phone can help you stay on track. Even one missed payment can drop your score by a lot.

2. Keep Credit Card Balances Low

Try not to carry high balances on your credit cards. This is called credit utilization—how much of your credit limit you’re using.

For example, if your limit is $5,000 and you’re carrying a balance of $4,000, that’s 80% utilization. That’s too high. You want to keep it below 30%, and under 10% is even better.

3. Don’t Close Old Accounts

Even if you’re not using an old credit card, keeping the account open can help your score. It adds to the length of your credit history, which lenders like to see.

Say you’ve had a card for 10 years. That long track record works in your favor. Cutting it off short may lower your average credit age.

4. Limit New Credit Applications

Every time you apply for a loan or credit card, the lender does a hard inquiry on your credit. Too many of these in a short time can hurt your score.

Only apply for credit when you really need it. If you’re shopping for a mortgage, do all your rate checks within a 30-day window. That way, it counts as just one inquiry.

5. Check Your Credit Reports for Mistakes

Sometimes credit reports include errors, like wrong balances, late payments that weren’t late, or accounts that aren’t even yours.

You can check your reports for free at AnnualCreditReport.com. Review all three: Experian, Equifax, and TransUnion. If you spot something wrong, you can dispute it online and get it fixed.

How Long Does It Take to See Results?

Improving your credit takes time, but it’s worth the effort. If you make consistent changes, you might see small improvements in a few months. Bigger jumps may take six months to a year, depending on your starting point.

Stick with it. Good habits add up.

Why This Matters for Your Mortgage

A better credit score gives you more loan choices. It can help you:

-

Qualify for a home loan

-

Get lower interest rates

-

Lower your monthly payment

-

Put less money down in some cases

Let’s say you get a 30-year mortgage for $300,000. If your interest rate is 6.5% instead of 7.5%, you could save over $60,000 during the life of the loan. That’s the power of a good score.

No Credit History or a Low Score?

If you’re starting from scratch, here are two simple ways to build credit:

-

Apply for a secured credit card – You deposit money up front, then use the card like normal.

-

Become an authorized user – Ask a family member to add you to one of their older credit cards. You get the benefit of their history without having to use the card.

Either way, start small and focus on consistency.

What To Do Next

If you're thinking about buying a home, now is the time to look at your credit. Visit AnnualCreditReport.com, check your score, and pick one or two tips to work on right away. Small changes can make a big difference when it’s time to apply for a mortgage.

Your future home—and your future self—will thank you.

|

or another way